No products in the cart.

Majority of Europe’s biggest music festivals now owned by four companies, study finds

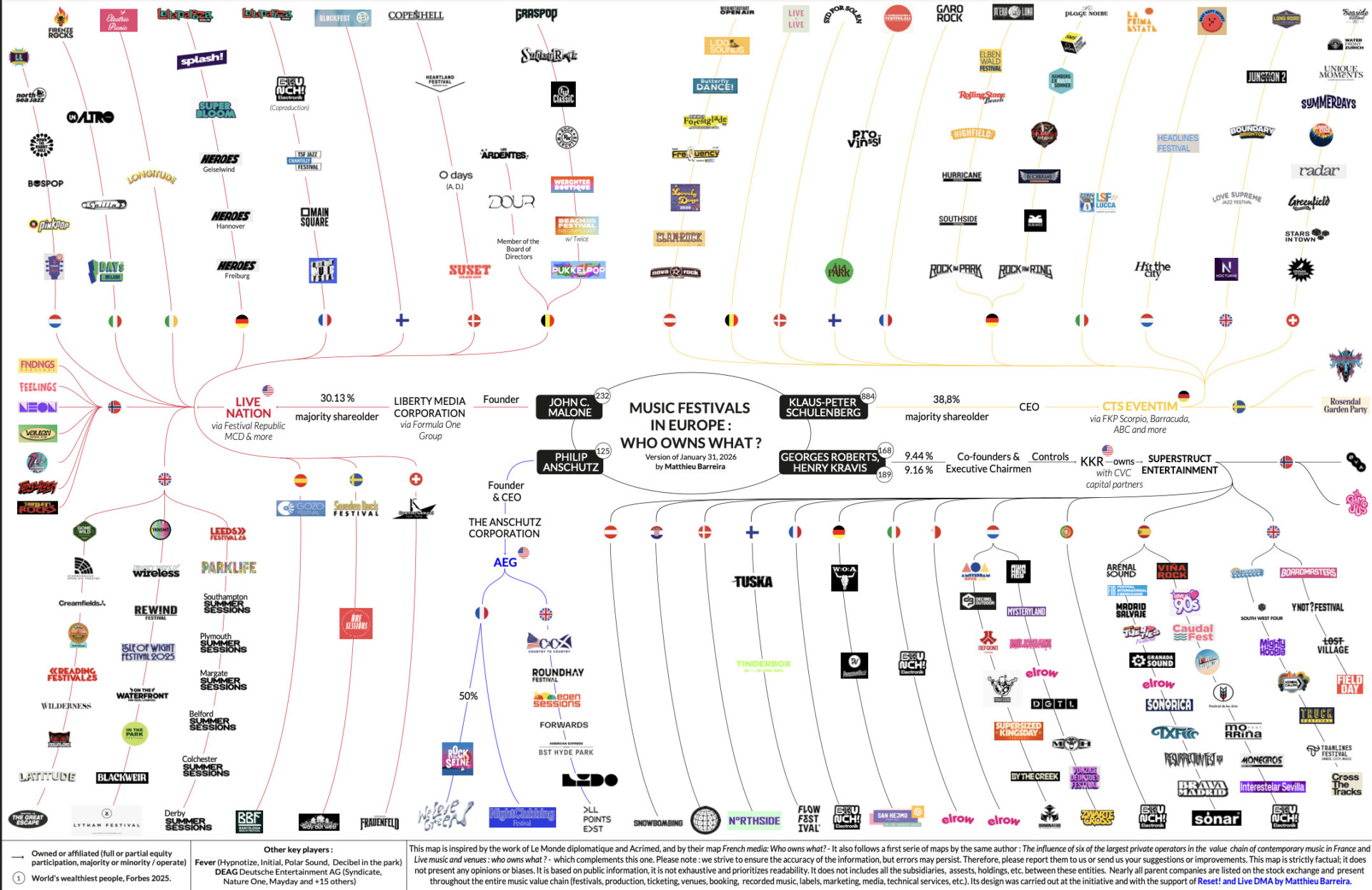

The majority of Europe’s biggest music festivals are now controlled by just four companies, according to a new study published by Live DMA and the Reset! network. More than 150 major festivals are now linked to AEG, Live Nation, CTS Eventim and Superstruct Entertainment, illustrating a growing concentration within the European live music sector.

Entitled Who Owns Europe’s Live Music Spaces?, the study was released on February 5 and is accompanied by two detailed maps—one focusing on festivals, the other on venues—aimed at making visible ownership structures that are often invisible to audiences, yet decisive in how the ecosystem operates.

“Behind many sold-out concerts and festivals, ownership structures remain largely invisible, even though they play a decisive role in how stages are operated, how risks are shared, and how revenues flow,” Live DMA and Reset! underline in their press release.

Four groups at the heart of the ecosystem

According to the festival ownership map, more than 150 of Europe’s largest events are linked to these four groups. Live Nation emerges as the most dominant actor, with around 120 subsidiaries operating across Europe and a global turnover estimated at $16.7 billion in 2022. CTS Eventim, meanwhile, generated close to €1.9 billion in revenue the same year, through ticketing, promotion and venue operations in more than 20 countries.

AEG Presents combines concert promotion with ownership of major infrastructures such as London’s O2 Arena or Berlin’s Mercedes-Benz Arena. Superstruct Entertainment, finally, owns and operates more than 80 festivals across ten countries in Europe and Australia. The group came under the control of private equity firm KKR, with CVC as co-investor, in 2024—an acquisition that sparked strong criticism due to the owners’ financial links to the arms industry, fossil fuel infrastructure projects, and companies operating in occupied Palestinian territories.

The study goes beyond a simple snapshot, highlighting an acceleration of this phenomenon in recent years. Between 2022 and 2025, the number of festivals linked to Superstruct rose from 34 to 63, those associated with CTS Eventim from 42 to 51, while Live Nation and AEG also strengthened their presence. This evolution confirms a structural trend rather than a temporary market adjustment.

Festivals now owned or operated by these groups include Wireless, Sónar, Reading & Leeds, elrow, Lollapalooza, Field Day, Latitude, Creamfields, All Points East and Junction 2, among others.

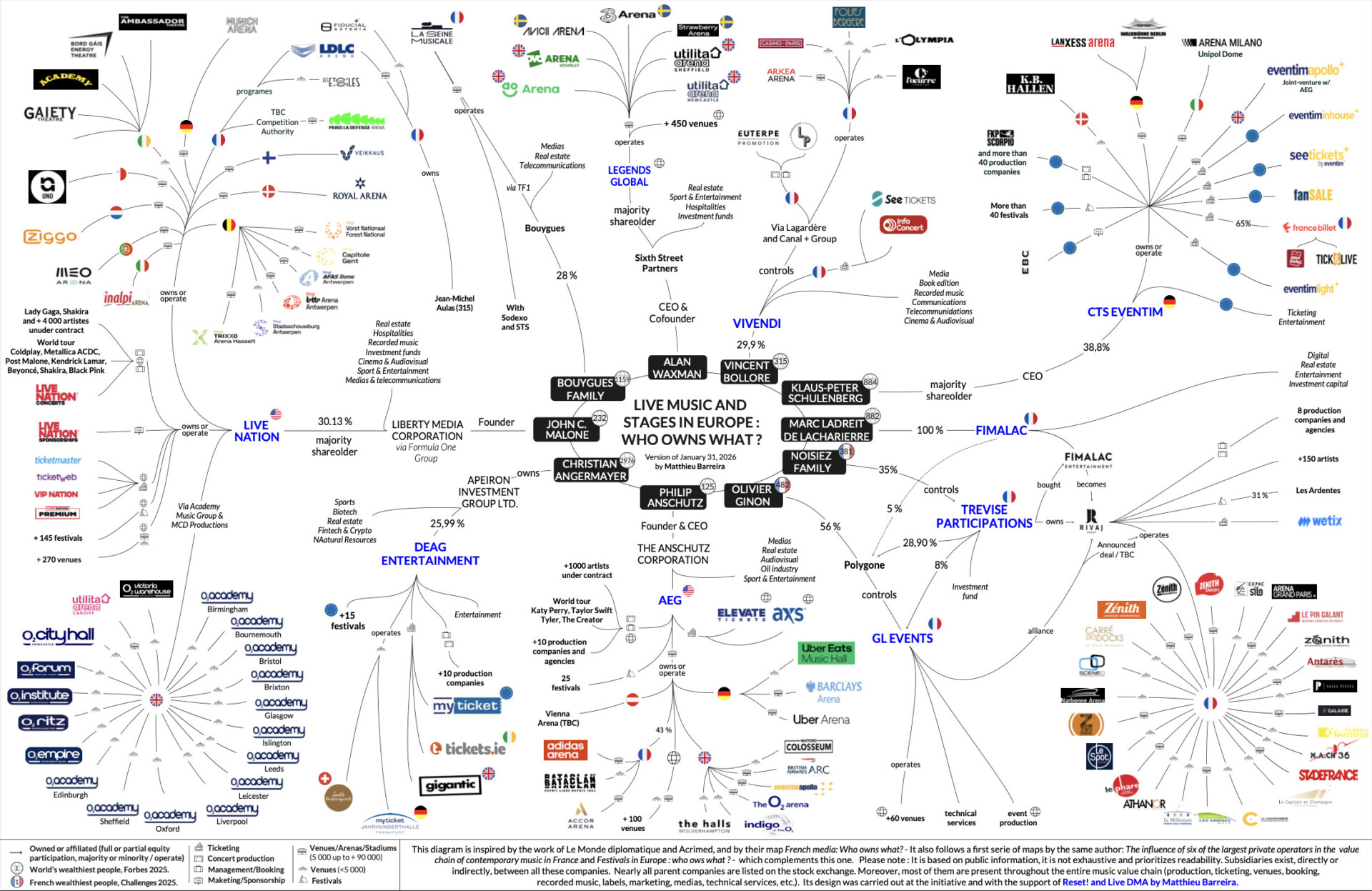

Festivals, venues and ticketing: different logics

The venue ownership map, however, paints a slightly different picture. While large corporations mainly concentrate their investments on arenas and stadiums—often integrated into real estate developments or multi-use complexes—the majority of small and medium-sized music venues remain independent, associative, municipal or locally owned.

The report also highlights the central role of ticketing within this configuration. Several major groups control or operate leading ticketing platforms, raising issues already documented in market analyses and political debates, particularly around speculative resale, access to high-demand events, and pricing practices.

This growing concentration has reignited concerns over its impact on cultural diversity and artistic independence. Emma Rafowicz, Member of the European Parliament and Vice-Chair of the Committee on Culture and Education, believes these dynamics call for a political response.

“More than ever, the concentration of the live music sector threatens cultural diversity and the independence of artists and producers,” she states, calling on the EU to limit vertical integration, separate certain activities along the value chain, and restrict the ownership of multiple events by a single operator, both within individual countries and across Europe.

Making visible the choices behind a ticket

Without claiming to be exhaustive, the maps published by Live DMA and Reset! primarily aim to make visible a reality that has long been underestimated. They invite institutions, professionals and audiences alike to reflect on the choices implied by every ticket purchased.

When we buy a ticket for a concert or a festival, who are we really supporting—and what kind of ecosystem do we want for live music in Europe?